On My Mind: Costs of Replication

Plus, framework for different ways to be contrarian

On My Mind

Costs of replication.

When looking at a business, one of my favorite things to think about are its costs of replication – that is, how hard would it be for another entity to reproduce the product being offered? That new entrant might be a startup looking to compete, or it could be a legacy company expanding to adjacent fields.

I typically bifurcate costs of replication into two parts: 1) the costs of production, and 2) the costs of everything else. Costs of production encompasses the things required to actually build and ship the product. “Everything else” might look like user acquisition, licensing, entrenched consumer bases, complexity of customer integrations, partner exclusivity agreements, proprietary data, and more.

Startups tend to emerge and succeed when incumbents’ defensibility is disproportionately weighted towards high costs of production, and then there is some disruptive force that makes it significantly easier to produce the product. A modern-day example might be defense tech: it historically required significant capex to produce the technology but now, with the capabilities of things like AI and advanced manufacturing, we are seeing a rise of new defense tech companies (“neoprimes”).

But it’s a double-edged sword. Lower costs of production may help startups get to market with less capital, but they also may make it easier for incumbents to fast follow. There’s a famous VC adage: “can the startup get distribution before the incumbent innovates?” The buffer that a startup may have had as its potential competitors were thinking through whether to allocate the resources to a buildout is now gone – the necessary internal resources (e.g. engineers) and time for a competitor to build the product have collapsed. Defensibility re-weights toward the “everything else” portion of replication.

I’ve been using this framing to think about where startups win vs. where incumbents can continue to compound. It’s especially relevant given the advances in AI. A product that used to take 5 engineers at 2 months to ship might now take one engineer, a massive token budget, and a few days to ship. In many categories, defensibility will increasingly shift from costs of building to deciding what to build and how to distribute it.

Frameworking

Peter Thiel has a famous framework for how to make money: a 4x4 of consensus vs. non-consensus, and being right vs. wrong. Being non-consensus and right leads to the most successful investments. Being consensus and right can still result in profitable outcomes, albeit often not nearly as big. And if you’re wrong, you lose money.

This week’s frameworking riffs on Thiel’s framework. It’s about how to be contrarian and, as a byproduct, the different ways to make money.

The opportunity to make a successful investment most often comes when there is space for people to change their minds. That shift – where one side switches their perspective – is often an important driver of changes in capital flows.

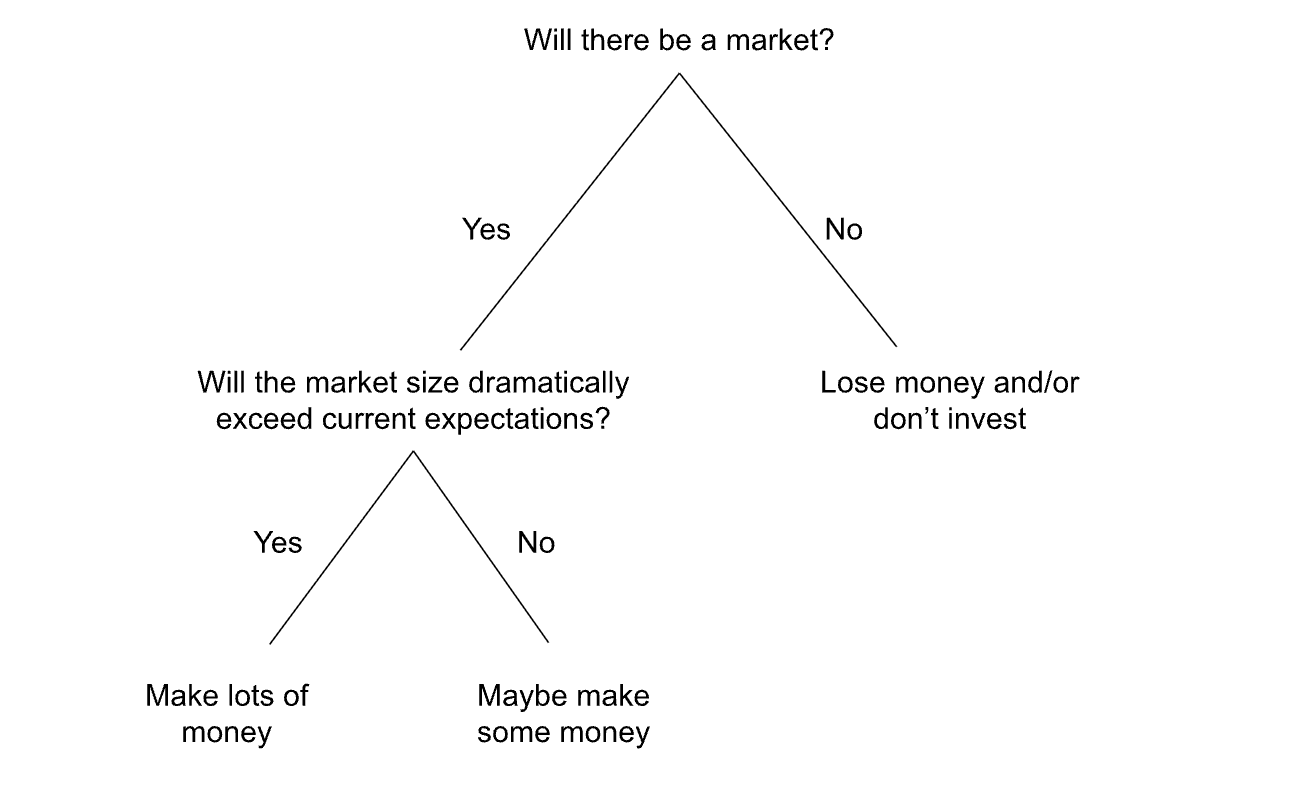

There are two ways to be contrarian. They can be visualized similar to a decision tree:

Step one: will a business exist? If many people believe that a business or market won’t exist – and then it does – there becomes a lot of room for people to change their minds.

Step two: everyone already agrees that a business or market will exist. The point of disagreement is about how big the business can get, or whether that growth is already priced in.

The first point of disagreement is frequently how early-stage venture capitalists make money. The latter is how growth-stage investors and (and some public market investors) tend to place bets.

In particular, betting that markets will be even larger than many believe is a core principle in underwriting extremely high P/E multiples. A fast-growing company in 2026 that trades at 100x TTM earnings is extremely expensive. But what if you believe their growth will double next year, then double again the year after that? That company is then trading at a 25x multiple using 2028’s earnings.

The most lucrative investments can come from being doubly contrarian, and doubly right – believing that a market will exist when others don’t, and then betting that it will get far larger than most people expect (even after everyone is in agreement that the market is large and valuable).

Content I Consumed this Week

Steve Carell on Amy Poehler’s Good Hang Podcast. Mafias and talent scenes are everywhere. I’m consistently amazed by the (largely comedic) talent that came out of Northwestern, and then Second City in Chicago, in the 1980s and 1990s. Tina Fey, Amy Poehler, Steve Carell, Julia Louis-Dreyfus, Stephen Colbert, Halle Berry, and so many more. It’s so cool to hear the stories about all of their early days, and Amy Poehler is such a good interviewer!

Marc by Sofia by Romy. While watching this, it occurred to me that I’ve maybe never seen a longer-form interview where the interviewer is Gen Z. Really enjoyed seeing the interaction between Sofia Coppola and her daughter Romy.

Why Florence Started the Renaissance by @tomaspueyo. Tomas’s blog, Uncharted Territories, is one of my favorite weekend reads. Every time I read one of his essays, I learn something new about how human civilization has evolved.

Books on the docket: The Infinity Machine by Sebastian Mallaby. If you’ve made it this far, please give me book recs!